How ERPNext Prevents Suspense Account Misuse in Bank Reconciliation

Using Suspense Accounts in bank reconciliation may balance books temporarily but creates risks. Learn how ERPNext prevents misuse via bank reconciliation.

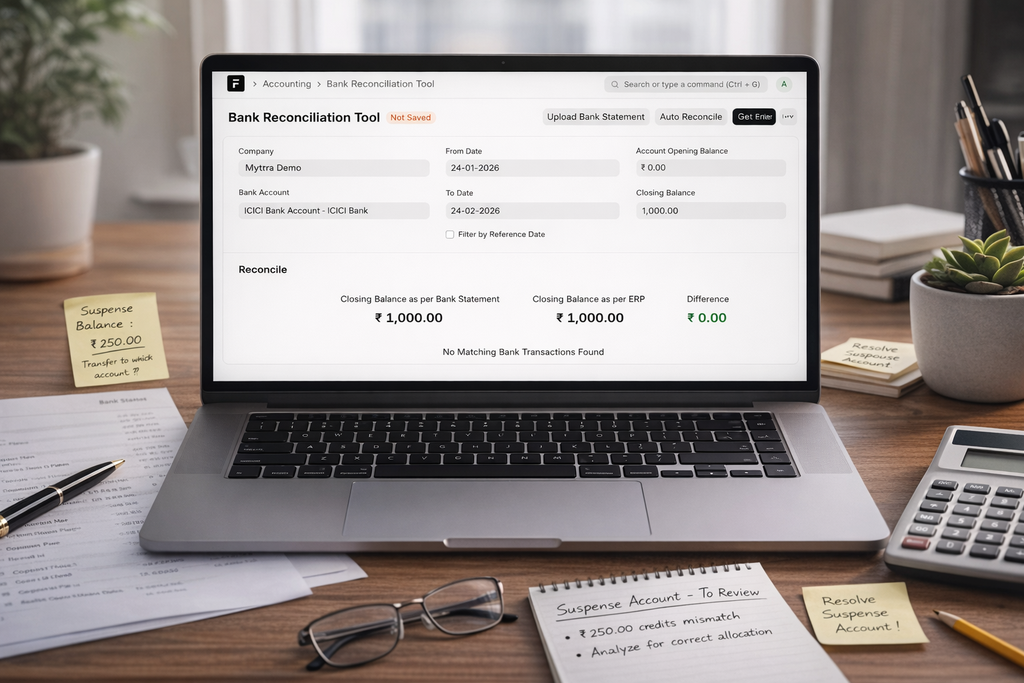

When accountants perform bank reconciliation, they sometimes encounter bank transactions that cannot be immediately classified. For example, a credit of ₹50,000 may appear without clear information about its source.

To force a balance match, some accountants record this as: Bank A/c Dr - To Suspense A/c. While this entry temporarily makes the books appear balanced, it does not represent proper accounting treatment. Posting unidentified transactions to a Suspense Account merely postpones classification and may lead to inaccuracies in financial reporting and audit complications.

What is a Suspense Account?

A Suspense Account is a temporary account used to hold transactions when there is uncertainty about proper classification. It is created to keep the accounting process moving while the true nature of a transaction is still being determined.

Suspense account is meant only for, temporary trial balance differences or posting errors while books are being finalized. It is not meant for unidentified Bank transactions.

Why Recording Unknown Bank Transactions in Suspense Is a Mistake?

A Suspense Account should not be a dumping ground for unidentified bank entries. Posting unknown transactions here is problematic because:

- It records entries without knowing their nature

- It may lead to incorrect profit figures as at the end of year the balance of suspense account is transferred to other income / expense

- It creates tax reporting errors as you miss to record the unidentified purchase invoices

- It raises audit issues

Accounting principles require that every entry must be supported by evidence and properly classified. Posting an unknown bank transaction to Suspense assumes classification has already happened, but it hasn’t.

How ERPNext’s Bank Reconciliation Tool Addresses This

The best solution is not posting to Suspense first, but identifying the transaction before recording it. ERPNext makes this easier with a structured reconciliation workflow.

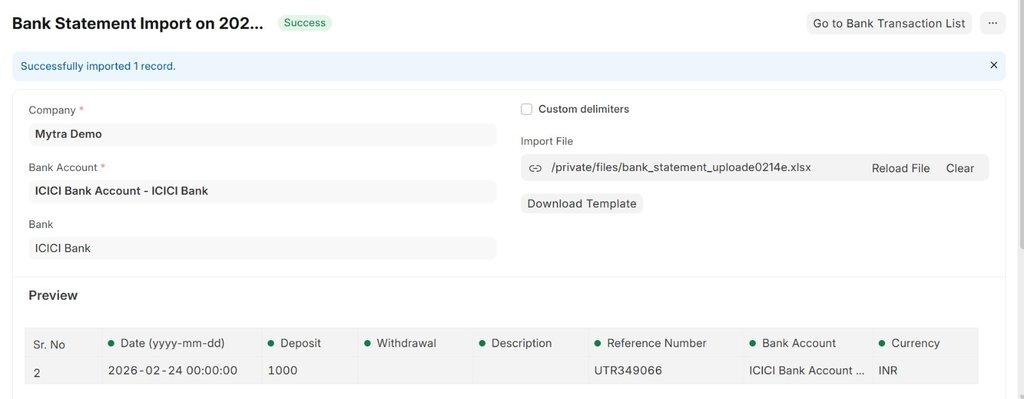

Step 1 : Import Bank Statement

Go to:

- Search Bank Statement Import in Awesome Search Bar

- Upload your statement (CSV/Excel)

- ERPNext records the bank movement but does not post to the General Ledger yet

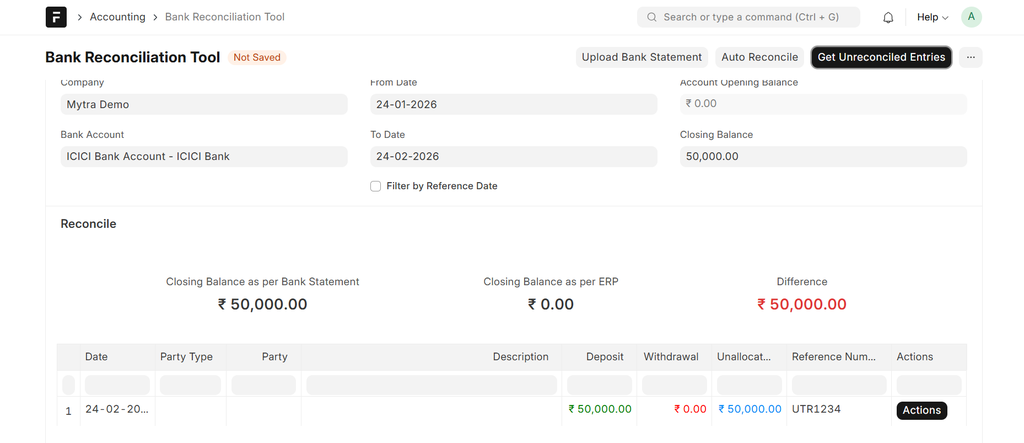

Step 2: Keep the Transaction Unreconciled

When the nature of a bank transaction is unclear, ERPNext does not force classification.

The transaction remains:

- In Unreconciled status

- Unallocated to any party or voucher

- Outside the Profit & Loss Statement

- Outside the Balance Sheet impact

This ensures that no incorrect accounting entry is passed until the transaction is properly identified, preserving financial accuracy and audit integrity.

Step 3: Reconcile by Creating Proper Entry

Once the nature is identified, reconciliation is ideally done by creating a new accounting entry. In ERPNext, this is typically handled by:

- Creating a new Payment Entry (PE) for customer or supplier transactions

- Creating a new Journal Entry (JE) for other types of receipts or payments

After creating the appropriate entry:

- ERPNext links it to the Bank Transaction

- The correct General Ledger impact is recorded

- Status changes to Reconciled

Only then does ERPNext post the correct accounting entry.

Conclusion

Matching a bank balance is not the same as proper accounting. The correct approach is to identify the true nature of every transaction before posting it in the books. ERPNext’s Bank Reconciliation Tool enforces this discipline by clearly separating the recording of bank movements from their accounting classification. While using a Suspense Account for unknown transactions may appear convenient, it merely conceals the underlying issue and can lead to financial inaccuracies.

By following ERPNext’s structured reconciliation process, transactions are not prematurely recorded, financial statements remain accurate, and audit as well as tax risks are significantly minimized. True bank reconciliation therefore means not just balance matching, but balance matching combined with correct classification.

Shalini Dondeti

ERP Software Developer

No comments yet. Login to start a new discussion Start a new discussion